Notes about the list of Singapore REITs data above:

- The data above is not real-time.

- Although we strive to keep the data as accurate as possible, we do not guarantee the accuracy of the data above. The information presented here is for general information only. It is not intended to be and does not constitute financial advice, investment advice, trading advice, or any other advice or recommendation of any sort. Please do your own research before investing.

How to Read the Data Above?

In the list above, we display all the REITs listed in the Singapore Exchange (SGX) and their unit price, dividend yield, price-to-book ratio (P/B), and gearing ratio (aggregate leverage ratio). The list is sorted alphabetically.

We mark some data with specific highlight colors, which indicate the following:

- RED: indicates the possibility of a red flag that needs more attention when analyzing the REIT further, for example, gearing ratio exceeding the regulatory limit, dividend suspension, etc.

- ORANGE: indicates the possibility of an issue that may be less than ideal. For example, the gearing ratio is getting very close to the regulatory limit, P/B is getting too low or high, and more.

- GREEN: indicates the possibility of a preferred state of that metric, for example, healthy gearing ratio, etc.

However, please note that the color markers above serve only as an indicator to nudge investors to investigate further when conducting their analysis. Please do not take the nudge at face value; always do your own research.

We also provide a more in-depth analysis and data for some of the blue-chips Singapore REITs, which you may find by clicking the REIT’s name in the list above. Here is the list:

| Name | Our Coverages |

|---|---|

| CapitaLand Ascendas REIT (CLAR)

SGX:A17U |

Analysis |

| CapitaLand Ascott Trust (CLAS)

SGX:HMN |

Analysis |

| CapitaLand Integrated Commercial Trust (CICT)

SGX:C38U |

Analysis |

| Frasers Centrepoint Trust (FCT)

SGX:J69U |

Analysis |

| Frasers Logistics & Commercial Trust (FLCT)

SGX:BUOU |

Analysis |

| Keppel DC REIT

SGX:AJBU |

Analysis |

| Keppel REIT

SGX:K71U |

Analysis |

| Lendlease Global Commercial REIT (LREIT)

SGX:JYEU |

Analysis |

| Mapletree Industrial Trust (MIT)

SGX:ME8U |

Analysis |

| Mapletree Logistics Trust (MLT)

SGX:M44U |

Analysis |

| Mapletree Pan Asia Commercial Trust (MPACT)

SGX:N2IU |

Analysis |

| Parkway Life Real Estate Investment Trust (PLife)

SGX:C2PU |

Analysis |

| Suntec Real Estate Investment Trust

SGX:T82U |

Analysis |

What is REIT (Real Estate Investment Trust)?

A REIT investment means your capital is pooled with other investors to acquire real estate. REIT invests in income-producing real-estates and distributes most of the profit to the shareholders. REITs are incentivized to distribute at least 90% of their taxable income yearly to their shareholders. For income-seeking investors, REIT is an asset class you may consider adding to your portfolio.

Types of REITs in Singapore

By Sectoral Exposure

Singapore REITs invest in various sectors, such as retail, office, healthcare, logistics, data centers, hospitality, etc. Investors can get exposure to multiple industries to diversify their risk factors associated with a single sector. For example, a downturn in the hospitality sector may not affect the data centers sector.

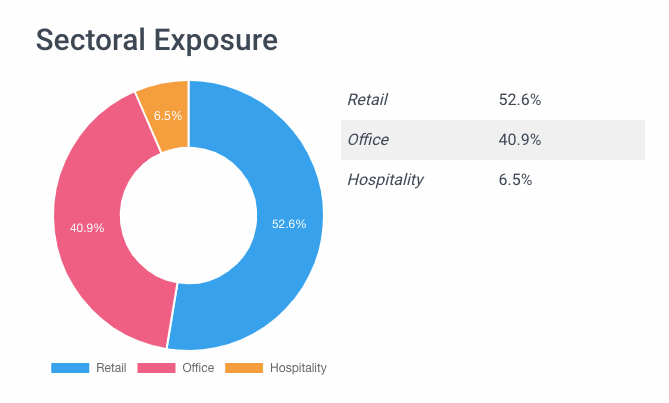

To learn more about the sectoral exposure for a particular REIT, you can visit the REIT’s details page from the list above. For example, here is the CapitaLand Integrated Commercial Trust (CICT) sectoral exposure chart from our CICT analysis page:

By Geographical Exposure

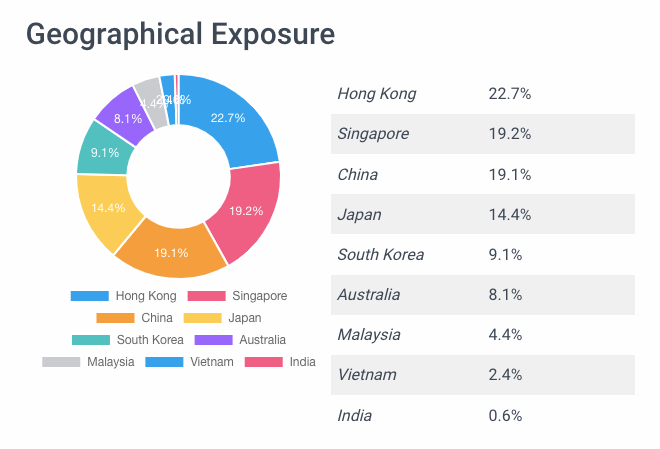

Different REITs offer different geographical exposures. Although all the REITs above are listed in Singapore, some have exposure to overseas markets. For example, Mapletree Logistics Trust (MLT) has exposure to nine countries: Hong Kong, Singapore, China, Japan, South Korea, Australia, Malaysia, Vietnam, and India. Although MLT is listed in SGX, the highest exposure is to the Hong Kong market, with Singapore only contributing to ~19% exposure.

Diversifying across multiple geographies will reduce your risk associated with specific countries/geographies. For example, a structural downturn in the US commercial property market caused many REITs with significant exposure to this sector and geography to be significantly impacted.

To reduce your overall risk, investors may consider diversifying their REIT portfolio across various industries and geographies.

Singapore REITs Pros

Income-Producing Asset

Most investors invest in Singapore REITs for distribution/dividends. All REITs are incentivized to distribute 90% of their income to their unitholders, and therefore, they are one of the favorite investment vehicles for income-seeking investors in Singapore.

From the list above, you may look at the dividend yield column to see the approximate percentage return per annum of the REITs return in the form of distribution/dividend.

Growing Dividends

The REIT’s distribution is primarily derived from the rental income it collects from its tenants. Because rental tends to increase along with the underlying economic fundamentals, the income the REITs collect also tends to increase over time. As a result, the REITs will be able to distribute growing dividends over time as their incomes grow.

Potential Capital Appreciation

While the primary emphasis might be on income distribution, many REITs tend to exhibit long-term value appreciation. This appreciation aligns with the overall health of the real estate sector in their specific geographic locations. With the potential for long-term capital appreciation and growing dividends, REITs can be an attractive proposition for income-seeking investors compared to bonds, which only offer fixed principal and interest.

Singapore REITs Cons

High Leverage and Debt

REITs are funded with debt. REITs use debt to finance their acquisitions and operations. The double-edged nature of debt and leverage in REITs means that while they can amplify returns, they can also exacerbate losses.

In a good economic environment, borrowing money to acquire more properties will provide investors with more rental income. However, when the market turns, the rental income may not be able to cover the loan that needs to be serviced.

Additionally, the property valuation may also decline, causing the lenders to no longer be comfortable offering any loan at competitive rates.

Because of leverage and debt, REITs generally are not considered the lowest-risk investments, as investors need to be comfortable with price and dividend fluctuations. Investors should be comfortable with this underlying risk before investing in REITs.

Highly Sensitive to Interest Rates

Because REITs use debt and leverage, they are susceptible to interest rate fluctuations. Most REITs usually have some portion of their debt hedged to fixed rates and some on floating rates. The floating component is vulnerable to interest rate movement as the impact is immediate. The fixed component is slightly better because the effect will only be felt upon refinancing. Regardless, even the fixed portion will eventually need to be refinanced and, therefore, exposed to the prevailing interest rate movement at the time of refinancing.

You may look at the REIT’s debt maturity profile to see how much debt needs to be refinanced yearly. If a significant chunk of the REIT’s debt needs to be refinanced soon with higher interest rates, you may expect the REIT’s borrowing cost to rise and create downward pressure on the REIT’s distribution.

As an illustration, if a REIT’s existing debt has an interest rate of 1.5%, but suddenly the interest rates shoot up to 3.5%, the cost to service the debt will also spike to account for the additional 2% rate increase, therefore causing the REIT’s net income and distribution to unitholders to decline. When you are highly leveraged, 2% will be quite significant.

Lower Leverage than Residential Properties

Although we have been addressing the issues with high leverage in Singapore REITs, the leverage amount is still below that of the residential property individuals can buy in Singapore.

For example, in Singapore, we only need to pay 25% of the downpayment and loan the remaining 75%. In other words, we also use debt and leverage to purchase our residential property. In this case, the leverage amount is even larger than Singapore REITs, which are regulated to only allow up to 50% for their aggregate leverage ratio.

But again, leverage is a double-edged sword, as we mentioned previously. It can be good and bad.

How to Buy REITs in Singapore?

REITs are tradable in the stock market and can be purchased just like how you buy a stock. If you want to buy Singapore REITs, you can use any stock broker with access to the Singapore Exchange (SGX). You may refer to our coverage of some of the best online brokerage accounts in Singapore and filter those with access to the Singapore Exchange.

What to Look for in Singapore REITs?

The table above displays some important metrics investors usually look for when assessing Singapore REITs. However, note that those are not comprehensive, and you should look at REIT’s portfolio and financial health holistically. Here are several metrics to pay attention to when looking at some REITs:

Dividend Yield

Most investors who own REITs in Singapore are usually in them for the dividend. Because REITs are mandated to distribute most of their income to the unit holders, this instrument is perfect for income-seeking investors who are bullish on the property sector but want to avoid owning and managing physical properties directly.

The dividend yield metric shows how much you will get from your principal as a percentage. For example, if you invest $10,000 into a REIT with a dividend yield of 5%, you will earn 5% * $10,000 = $500 annually.

In general, investors prefer a higher dividend yield. However, an unusually high dividend yield could be a red flag as it may indicate something unusual is happening with the REIT. The dividend yield will shoot up if the REIT unit price drops significantly. But this is likely not a good thing as the price drop reflects the market pricing in (potential) problem with the REIT. Instead of just looking for a high dividend, investors should look for a sustainable dividend with a continuous track record of dividend growth.

Price-to-Book (P/B)

P/B is a ratio of the REIT price divided by its book value per unit. The book value (or net asset value) is the total assets minus the total liabilities. A P/B below 1 may indicate an undervalued REIT unit price, while a P/B value above 1 may indicate an overvalued unit price. However, please also take note of the historical P/B ratio and sectoral data because some REITs can command higher P/B ratios due to their sectors, quality, and other business moats.

An abnormally low P/B ratio may also indicate something unusual with the REIT. You should investigate further to determine what causes the irregularity.

Gearing Ratio / Aggregate Leverage Ratio

The gearing or aggregate leverage ratio measures the REIT’s financial leverage. The gearing ratio is calculated as the total debts divided by the total assets. A lower number means the REIT uses less leverage, which usually translates to less volatility from the interest rate fluctuation. REIT investors typically pay close attention to this number to ensure the REIT does not over-leverage itself. Singapore REITs need to maintain a gearing ratio of < 50%. REIT’s adjusted interest coverage ratio (ICR) is lower than 2.5x; the ratio is capped at only 45%. If a REIT exceeds the maximum leverage ratio, it must do whatever it takes to lower this ratio to strengthen its financial position. This action may not be preferable to investors, such as more equity financing (which can cause dilution), portfolio divestments (which may potentially lower the REIT’s distribution), distribution suspension, or even REIT’s dissolution.

This scenario usually happens during a high-interest-rate environment where borrowing costs become more expensive. At the same time, the property valuation may decline as there is less demand due to the high interest rate. As a result, the gearing ratio will rise when the property valuation decreases while the debts increase from the higher borrowing costs.

It is generally good to look for REITs with lower gearing ratios to provide enough buffer should the property market deteriorate in the future. A lower gearing ratio also implies lower interest expense from the debt and more headroom for future acquisition.

Debt Maturity Profile and Refinancing

All Singapore REITs are financed with debts. The details of how the REIT finances the debts are crucial. A well-managed REIT should have a higher percentage of its debts funded with a fixed interest rate, with the maturity staggered over the next several years.

Borrowing with a fixed interest rate allows the REIT to manage its finances better because it is generally more predictable. Fixed rates also enable the REIT to minimize the short-term impact of interest rate volatility.

Even with a fixed rate borrowing, eventually, the REIT will need to refinance its debts. This refinancing risk is why it is also essential that REIT’s debt maturity is staggered. When they need to refinance their maturing debts, they must refinance at the prevailing interest rate at the time of the refinancing. Should interest rates rise, refinancing will become more expensive. If a big chunk of their debts matures around the same time, they will be exposed to this interest rate risk. A well-managed REIT usually has a roughly equal debt maturing over the next several years. This is similar to the concept of bond laddering but applied to borrowing.

Portfolio and Geographical Exposure

Different REITs hold different real estate portfolios at various locations. Some REITs own shopping malls, while some own hospitals. Some focus on the Singapore market, while others are more geographically distributed.

The performance of various real estate types can vary depending on the market cycle. At the same time, different countries may be in different market cycles, causing their performance to vary. As investors, diving deeper into the REIT portfolio holdings and their geographical exposure allows us to understand better the potential risks associated with the REIT.

Occupancy Rate and Tenant Profile

At the core of REIT’s income is the rent it receives from its tenants. A low occupancy rate is a cause for concern because it usually translates to lower rental income. A consistently high occupancy rate indicates strong demand for the REIT’s portfolio. Investors in REITs should pay attention to the occupancy rate and any potential downward trend that could be cause for concern.

The tenant profile shows how well the REIT can secure tenants with diversification in mind. For example, if a REIT only has a single tenant from one industry, the REIT occupancy rate may be significantly affected if the sector faces a downturn.

The REIT metrics discussed above offer a foundational framework for analysis but are by no means exhaustive in their coverage of all relevant factors. Please make sure you learn more about REIT before investing so that you are fully aware of the risks associated with investing in REIT.

The table above provides general information about Singapore REITs to get you started. Due to the evergreen nature of the Singapore property market, Singapore REITs are a popular investment choice for investors. However, please be aware that REIT carries a different risk profile than owning a physical residential property.

If you want to invest in Singapore REITs but prefer a more ‘passive’ investing style, you may consider investing in Singapore REIT ETF. By investing in REIT ETF, the ETF manager will do most of the hard work for you. Happy Investing!