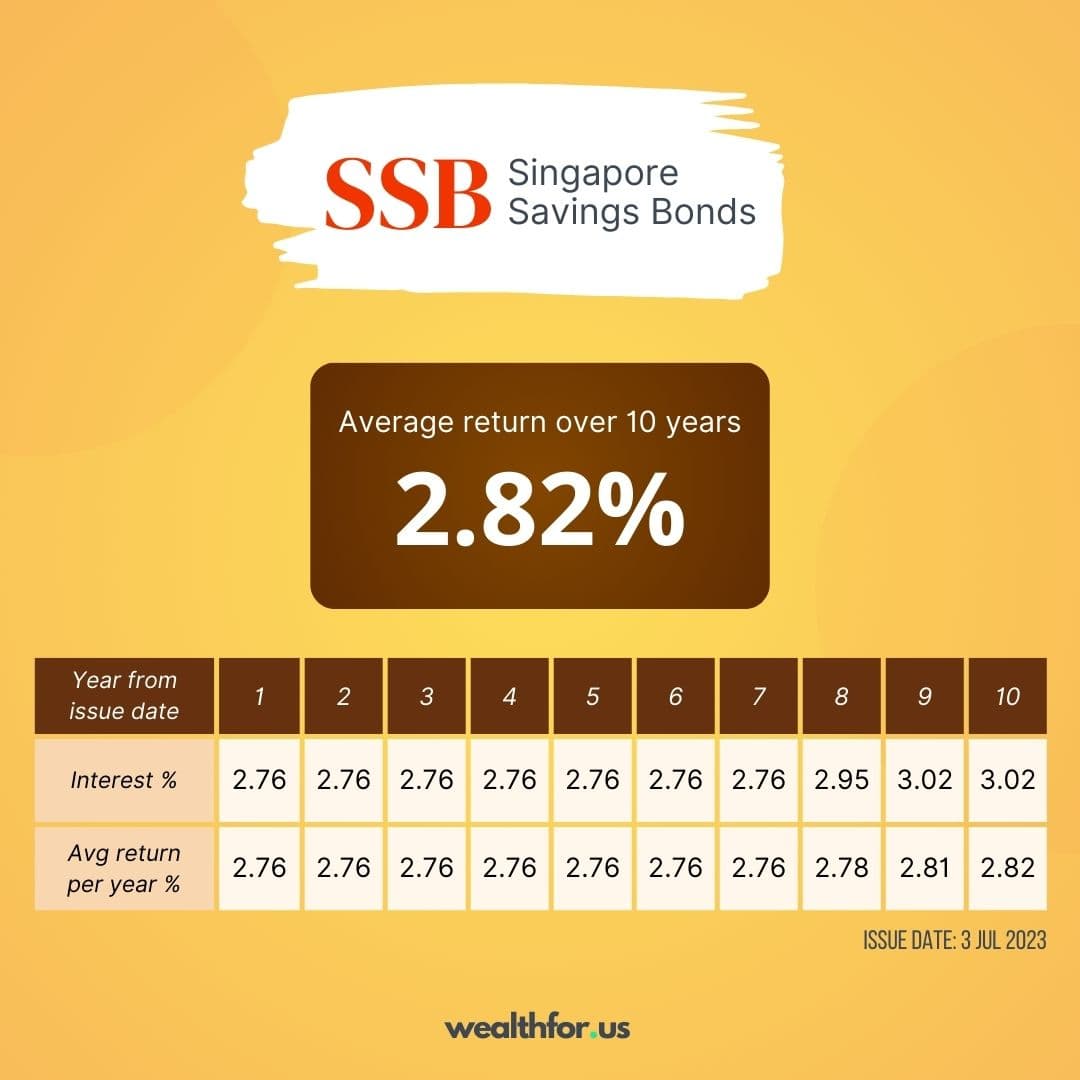

The latest Singapore Savings Bond SSB July 2023 offering is released, and the average 10-year yield is 2.82%, with the first-year yield at 2.76%. Just like the previous month, this month’s offering is somewhat lackluster. With the interest rate continuing to decline, is SSB still worth considering?

Key Takeaways

- SSB July 2023 10-year average rate is roughly flat, but the 1st-year rate is much lower.

- Short-term investors should consider alternatives such as t-bills, cash management accounts, or high-yield savings accounts.

- Long-term investors may consider locking in the relatively higher interest rate now as the trend continues to decline.

- This month’s offering can be an excellent chance to recycle older SSB yielding less than 2.76%.

What’s in SSB July 2023 Offering?

Here is the summary of this SSB July 2023 issuance:

Overall, with the average 10-year return roughly the same as last month’s issuance but with a lower first-year rate, we have to say that this month’s offering is not that attractive.

While the general trend of the long-term interest rate is down, we have seen a recent slight bump in this long-term interest rate. Many factors could be in play, such as sticky inflation, debt ceiling issue, stronger-than-expected economy, etc. This bump is reflected in this month’s SSB July 2023 issuance with a higher yield for years 8 to 10.

If you are interested in buying this SSB July 2023, take note of the following application timeline:

| Opening Date | 1 Jun 2023, 6 pm |

| Closing Date | 26 Jun 2023, 9 pm |

| Allotment Date | 27 Jun 2023, after 3 pm |

| Issuance Date | 3 Jul 2023 (by the end of the day) |

You can then follow our step-by-step guide on how to buy SSB.

Declining Demand

We have seen from several past issuances that the demand for SSB has steadily declined. All 2023 issuances saw low demand, with most applicants getting full allocation or a high-enough ceiling. With the relatively low first-year rate, this trend of low demand may continue in this month’s issuance. There is a good chance that this month will also be undersubscribed.

Is SSB Still a Good Buy?

The main attraction of SSB is its long-term maturity but with the flexibility to withdraw early any month without penalty. You even get the accrued interest. Because you can redeem early, should the interest rate goes up, you can redeem an older SSB yielding lower and buy newer issuance with a higher rate. If the interest rate decreases, you can keep your existing SSB and earn higher rates until maturity. If this flexibility is what you are looking for, you may consider SSB in your portfolio.

For Long-Term Bond Investors

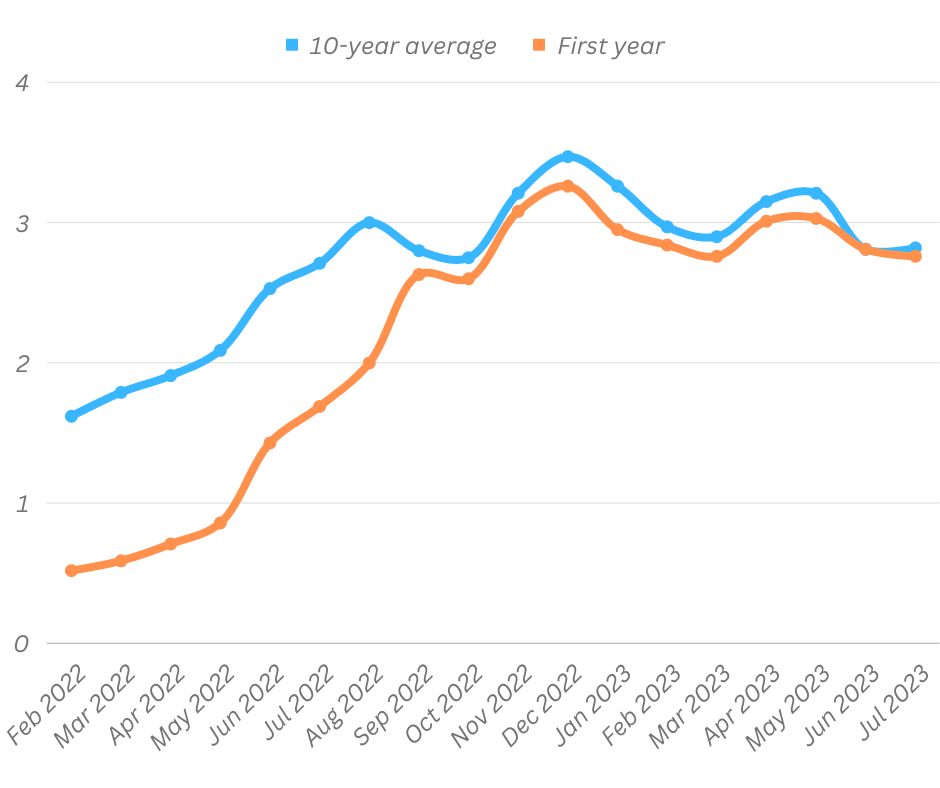

Though the rate is on the way down, note that it is still one of the highest in recent times.

As we can see from the chart, the current rate is still relatively attractive if we compare it to the rate even just from early 2022. With the market expecting us to be at the tail-end of the current interest rate hike cycle, this could be your chance to lock in the current rate for the next ten years.

For Shorter-Term Investors: Other Fixed Income Alternatives

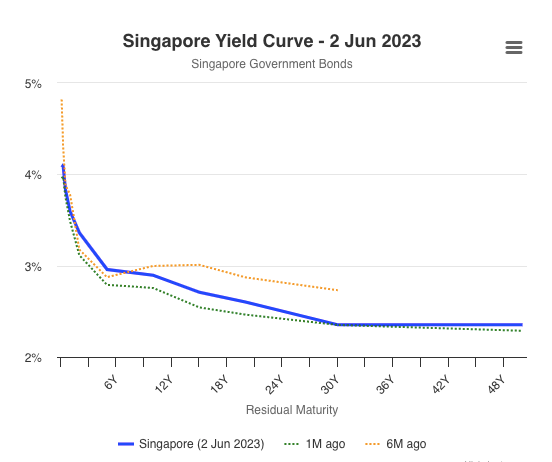

Our yield curve is currently inverted, meaning the short-term interest rate is higher than the long-term interest rate.

To benefit from this inverted yield curve, investors may consider a mix of short and long-term fixed-income instruments to capture the higher short-term interest rate. A combination of SSB and shorter-term instruments such as t-bills, fixed deposits, cash management accounts, and high-yield savings accounts can be a viable solution for most investors.

For investors looking to park their cash in the short term, many alternatives yield higher than SSB, such as T-bill, high-yield savings, and cash management accounts. These instruments currently still yield higher than 3.5%, which is significantly more than SSB July 2023 1st year rate of 2.76%. With the current interest rate offering, we believe SSB is no longer an attractive option for parking short-term cash.

Recycle Older SSB

If you have an older SSB yielding less than 2.76%, this month can be the perfect opportunity to recycle to the new SSB. As we expect the demand to be low, you can recycle your older SSB without worrying about hitting the ceiling from this month’s auction.

What Would We Do?

We have been buying SSB when the interest rate was above 3% and optimizing our long-term allocation during that period. Therefore, we will not be adding SSB anymore this month.

We use a mix of t-bills, cash management, and high-yield savings accounts for parking short-term cash.

Follow us on Twitter to stay up-to-date:

The latest SSB offering yields 10 year avg of 2.82%.

The first year rate is 2.76%.

The rate is pretty much flat from last month. But it is still one of the highest in recent years. pic.twitter.com/mg1PpoIGXc

— wealthfor.us (@wealthfor_us) June 1, 2023