The latest 6-month T-bill auction on 25 May was good news for investors: the cut-off yield jumped to 3.85%. While the fixed deposit rates started declining, the Singapore t-bill yield rebounded. Yay! What’s driving the rebound on the yield, and should we invest in T-bill?

T-bill Demand Rebounded

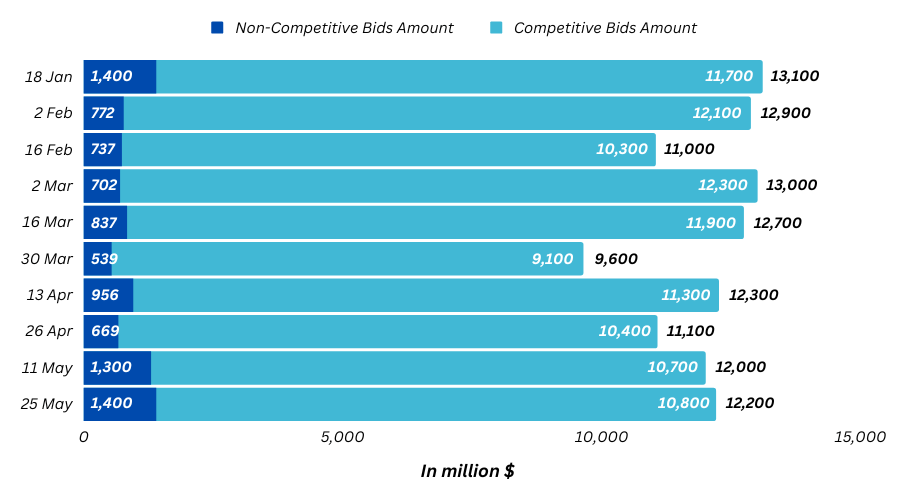

The last T-bill application amount went up to $12.2 billion (up slightly from $12 billion from the previous auction). Though not significant, the rise in demand is still surprising to investors because of the trend of lower interest rates and the possibility of losing a one-month CPF interest rate due to the unfavorable maturity date.

The T-bill demand rise may be partially attributed to the lower interest rate alternative from the fixed deposits, which have steadily declined in the past few months. This higher demand may contribute to a slight rebound in the final cut-off yield.

Larger T-bill Allotment Size

This last T-bill auction saw a total allotment amount of $5.3 billion, slightly higher than the previous issuance amount of $5 billion. The slight bump in the allotment size may contribute to the higher cut-off yield as more bids receive their allocation.

US Interest Rate Rising & Market Expectation

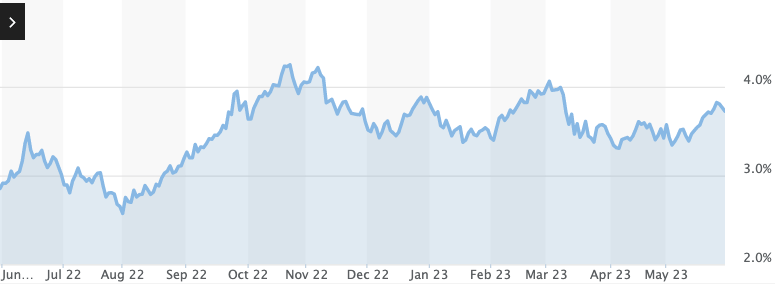

The rebound in Singapore T-bill yield was unsurprising considering the recent rise in the short-term and long-term US treasury rates.

Many factors were in play: the debt ceiling issue, the growing US economy, the sticky inflation, the Fed that keeps increasing rates, and the market not expecting interest rate cuts so early.

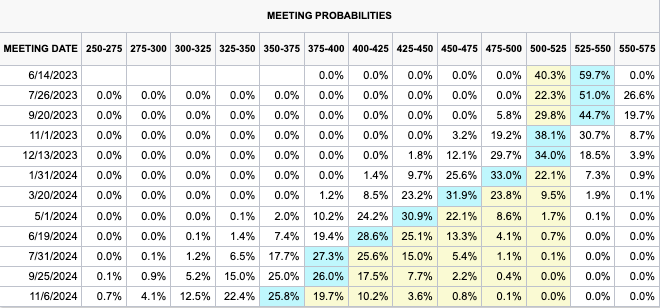

With the market generally not expecting interest rate cuts anytime soon and expecting the higher interest to stay, it is surprising for the Singapore local banks to cut their fixed deposit rates so quickly. The T-bill auction result shows that the market still demands higher short-term rates, at least for now.

Should We Invest in T-bills? Better than Fixed Deposits?

Many T-bills alternatives, such as cash management and high-yield savings accounts, yield higher than the latest cut-off yield of 3.85%. However, with these alternatives, there is usually a ‘catch.’ For example, some cash management accounts with higher interest do not guarantee your initial capital. High-yield savings accounts have many hoops you need to get through to receive the highest possible interest rate, thus rendering the effective interest rate much lower. Additionally, there is a limit on the amount you can put into the savings account to receive that high-interest rate.

T-bill has no ‘catch’ because the initial principal and interest are guaranteed for the whole duration regardless of market volatility. There is also a very high ceiling on the amount you can buy. You can buy as much as you want (subject to allotment size). With such characteristics, therefore, the best comparison to T-bill is the fixed deposit.

With the T-bills yielding much higher than the fixed deposits, there is little reason to park your cash in fixed deposits. T-bill is just more attractive at the moment. And, if you want to be sure, you can use the competitive bid when applying for T-bill to ensure you will get the rates you can accept.