CapitaLand Integrated Commercial Trust (CICT) has just released its FY2023 financial results. Let’s look into CICT Q4 2023 results to see how it performed last quarter.

CICT is Singapore’s first and largest REIT, with exposure to the office and retail sectors in Singapore, Australia, and Germany.

Financial Performance

In the table below, we compare CICT FY2023 vs. FY2022 results:

| FY2023 | FY2022 | Change | |

|---|---|---|---|

| Gross Revenue | $1,559.9m | $1,441.7m | +8.2% |

| Operating Expenses | $444.0m | $398.4m | +11.45% |

| Net Property Income | $1,115.9m | $1,043.3 | +7.0% |

| Distributable Income | $715.5m | $702.4m | +1.87% |

| DPU | 10.75 cents | 10.58 cents | +1.61% |

Gross revenue climbed by 8.2% YoY from $1.44 billion to $1.56 billion but was offset by higher operating expenses, which also jumped by 11.45%. The net property income grew 7% YoY to $1.12 billion. Revenue growth can be attributed to the full-year contributions from recent acquisitions in 2022 and the higher rental income from existing properties.

As a result, CICT managed to increase its DPU slightly by 1.6% YoY from 10.58 cents to 10.75 cents, a welcome news given the current economic climate. Overall, CICT’s financial performance looks stable.

Debt Profile

Here we compare CICT Q4 2023 vs. Q3 2023 debt profiles:

| Q4 2023 | Q3 2023 | Change | |

|---|---|---|---|

| Aggregate Leverage Ratio | 39.9% | 40.8% | -0.9% |

| % of Borrowings on Fixed Interest Rate | 78% | 78% | N/A |

| Interest Coverage Ratio | 3.1x | 3.1x | N/A |

| Average Cost of Debt | 3.4% | 3.3% | +0.1% |

CICT’s debt profile looks relatively healthy. We saw an improvement in its aggregate leverage ratio by 0.9% to 39.9%. The percentage of borrowings hedged to a fixed rate was stable at 78%. Notably, the interest coverage ratio has stabilized at 3.1x, halting the declining trend observed in previous quarters. Overall, we like CICT’s debt profile and think CICT should be able to weather any prolonged higher interest rate environment.

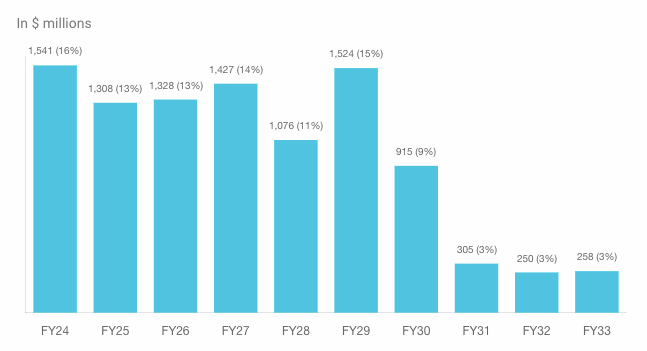

Debt Maturity Distribution

Despite the expected rate cuts, the market expects the interest rate to remain elevated this year and next. The good news is that CICT has a well-distributed debt maturity distribution, with only 16% due for refinancing in 2024 and 13% in 2025. We can see from the chart that there are only around 11-15% of refinancing obligations every year until 2030.

We think CICT’s debt maturity distribution is well spread out enough that it should be able to weather the current higher interest environment.

Portfolio Occupancy

Here is the summary of CICT portfolio occupancy metrics:

| Q4 2023 | Q3 2023 | |

|---|---|---|

| Portfolio Occupancy | 97.3% | 97.3% |

| WALE | 3.4 years | 3.5 years |

Again, we can see a solid portfolio occupancy rate for CICT. Both the portfolio occupancy and the WALE were stable last quarter. CICT also recorded FY2023 positive rental reversions of 8.5% for its retail and 9% for its office portfolios.

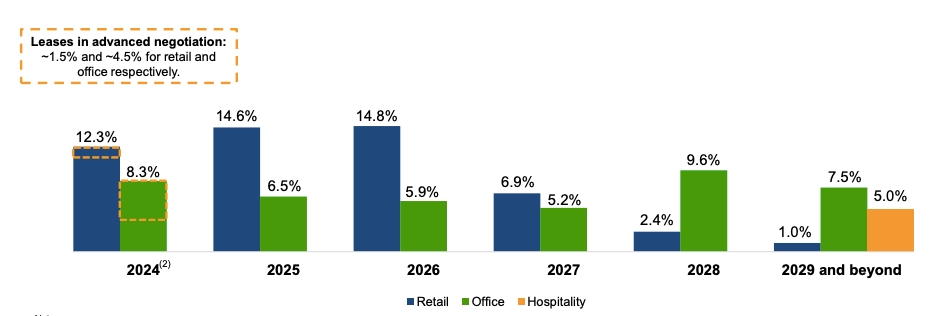

For its lease expiry, it is pretty well spread out over the next several years. However, it is worth noting that about 40% of leases are due for renewal within the next two years.

Remarks

As expected, CICT’s financial performance was stable last quarter. Despite the challenging economic environment, CICT still managed to grow its revenue and net property income by 8.2% and 7.0%, respectively. CICT DPU climbed by 1.6% YoY to 10.75 cents for FY2023.

CICT’s debt profile also strengthened slightly last quarter, with the aggregate leverage ratio decreasing to 39.9%. The debt maturity profile was also healthy, with only 16% refinancing obligation due in 2024 and 13% due in 2025.

Coupled with its strong portfolio occupancy profile, we think CICT is well-equipped to weather any prolonged higher interest environment that is expected to last longer throughout 2024 and possibly 2025.

If you are a CICT unitholder, the DPU for H2 2023 is 5.45 cents. Please take note of the following dividend dates:

| Ex-dividend Date | 14 Feb 2024 |

| Record Date | 15 Feb 2024 |

| Payout Date | 28 Mar 2024 |

CICT has a dividend yield of 5.3% and a price-to-book ratio of 0.95. To learn more about CICT, please visit our CICT analysis page and our CICT dividend page.

You may also check out our Singapore REITs page to analyze other REITs.