The year 2024 was phenomenal for Singapore stocks, with the Straits Times Index (STI) hitting a 17-year high. Yet, not everything is rosy. Beneath the surface, there is a growing divide in performance between the two main sectors inside the index: Banks and REITs. What happened, and what can we expect going forward?

What Happened?

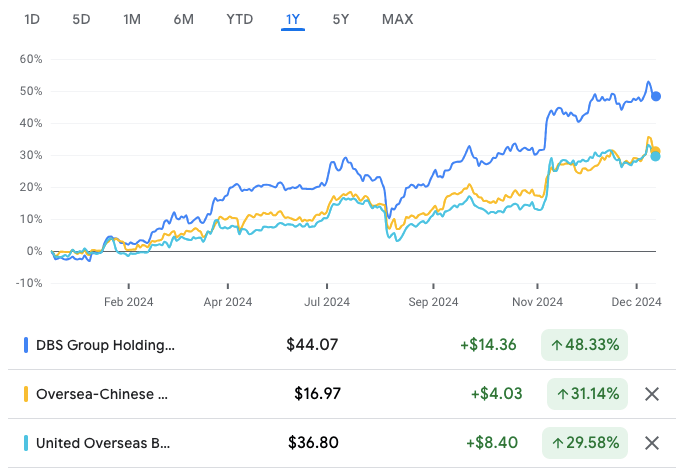

Let’s look into the chart. Here is the performance of the Singapore banks in 2024:

All three Singapore banks performed exceptionally well in 2024 and ended the year significantly higher (~30% to ~50%). This performance is fantastic, and do not forget that they also pay a >4% p.a. dividend.

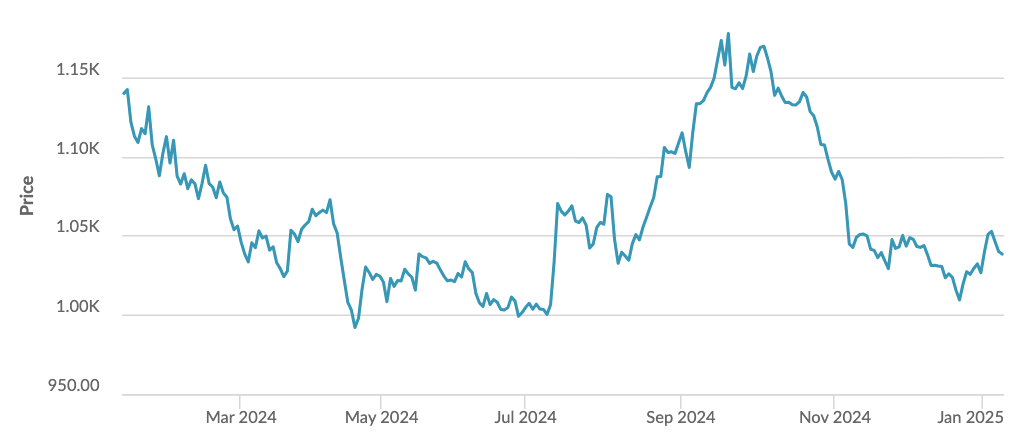

On the other hand, here is the chart for the iEdge S-REIT Leaders Index, which comprises the largest blue chip REITs listed in Singapore:

The REIT index was down ~10%. Even with the dividend payouts, it is still down on the year. Some REITs with exposure to overseas property markets performed even worse. The performance of the banks and the REIT was the opposite. What happened?

The answer is the future interest rate expectation.

How does interest rate impact Banks and REITs?

One of the revenue sources for banks is the net interest margin (NIM). NIM is the net income from the interest it receives from credit products (e.g., home loans) minus the interest it pays to deposit holders (e.g., fixed deposits and savings accounts), expressed as a percentage.

A higher interest rate usually means higher NIM and income for banks. Lower interest rates typically compress the NIM and lower bank income.

For REITs, interest rate directly impacts their borrowing costs. REITs are usually highly leveraged, which means they borrow a lot of money to acquire properties. If the interest rate is high, REITs must borrow and pay higher interest, and vice versa. Higher borrowing cost means lower income and distribution given to unit holders.

Given the relationship between interest rates and the two sectors above, you can probably guess why they performed in opposite directions. Yes, although the Fed has initiated its rate-cut cycle, there is an expectation that the pace of the rate cuts will be slower than expected. Interest rate is expected to stay higher for longer.

Banks, which generate income from interest rates, benefit from a prolonged period of higher interest rates. Conversely, REITs, which must borrow at higher rates, are negatively affected by this scenario.

Interest Rates Projection in 2025

So far, the Fed has reduced the federal funds rate by one percentage point over three meetings in September, November, and December 2024. As of January 2025, the rate is 4.25%–4.50%. This is no surprise, as all these cuts were already expected.

If so, why do REITs continue to sell off while the banks continue to perform well?

The answer lies in future interest rate expectations. As indicated in its latest FOMC meeting, the Fed has revised its 2025 projection from 4 rate cuts to 2.

Many factors contribute to the slower expectation of rate cuts. These include sticky inflation, a strong US economy, a robust job market, and a resilient GDP that continues to grow despite the challenges of higher interest rates. The strong US economy allows the Fed to maintain higher interest rates for an extended period to ensure inflation is fully contained.

Banks & REITs Valuation

Given the expectation that a higher interest rate environment will persist longer, should we consider Banks or REITs? Let’s examine their valuations.

Banks Valuation

Here is the summary of the three Singapore banks’ valuations.

| P/B Ratio | 10-Yr Historical Median P/B Ratio | P/E Ratio | 13-Yr Historical Median P/E Ratio | |

|---|---|---|---|---|

| DBS | 1.87 | 1.33 | 11.46 | 11.25 |

| OCBC | 1.34 | 1.08 | 10.31 | 10.33 |

| UOB | 1.3 | 1.1 | 11.03 | 11.17 |

The price-to-book (P/B) ratio is commonly used to assess a bank’s valuation. The table shows that all three banks’ P/B ratios are significantly higher than their historical values.

Looking at their price-to-earnings (P/E) ratio, they are roughly in line with the historical median values, indicating a fair valuation.

In summary, the three Singapore banks seem ‘overvalued’ at the current price level. However, this does not mean the price cannot go even higher. Given the expected higher interest rate environment, banks will continue to enjoy the higher NIM this year. However, with the interest rate expected to decline further in the long term, the long-term risk-reward ratio does not seem to be in investors’ favor at the current valuation.

REITs Valuation

How about REITs? Here are some of the largest REITs in Singapore:

| P/B Ratio | 10-Yr Historical Median P/B Ratio | |

|---|---|---|

| CapitaLand Ascendas REIT | 1.11 | 1.19 |

| CapitaLand Integrated Commerical Trust | 0.91 | 1.05 |

| Frasers Centrepoint Trust Trust | 0.93 | 1.05 |

| Mapletree Industrial Trust | 1.23 | 1.31 |

| Mapletree Logistics Trust | 0.87 | 1.05 |

| Mapletree Pan Asia Commercial Trust | 0.68 | 1.12 |

Like banks, we like using the P/B ratio to estimate a REIT’s valuation. The table above shows variation among the REITs, with some seemingly ‘undervalued’ and some ‘fairly-valued.’

Before you rush into those ‘undervalued’ REITs, please know that the lower P/B ratio may indicate potential challenges facing the REIT itself.

For example, the Mapletree Pan Asia Commercial Trust (MPACT) has a much lower P/B ratio than its historical median value. So it is cheap, right? Well, it depends on whether you think the risks associated with the REIT have been priced in and the REIT is on the verge of a turnaround.

MPACT has significant exposure to overseas markets, namely the China and Hong Kong markets, which have performed poorly recently. With the economies in those regions not doing well, rental income has experienced a negative reversion and has yet to recover.

As prudent investors, we must do our due diligence before investing in any asset.

What Do We Do?

With the interest rate expected to decline in the future and the rich valuation of the local banks, we do not plan to acquire any of them at the moment. However, we believe that the three local banks are fundamentally great businesses, and we would be happy to add more positions should a better opportunity arise.

As for the Singapore REITs, barring any black-swan event such as a major recession, we believe the sector’s turnaround may occur in the next several quarters as more debts are refinanced at higher rates and borrowing costs stabilize.

Despite that, we are still cautious and are only interested in some of the strongest blue-chip REITs, which are in a stronger position to weather any economic scenario. Additionally, we will track the rental reversion of some of these REITs to assess potential upcoming challenges if the rental reversion stays negative.

What do you think? Are you interested in any of the local banks or the REITs?

Please visit our Singapore REITs data page for further information on Singapore REITs.