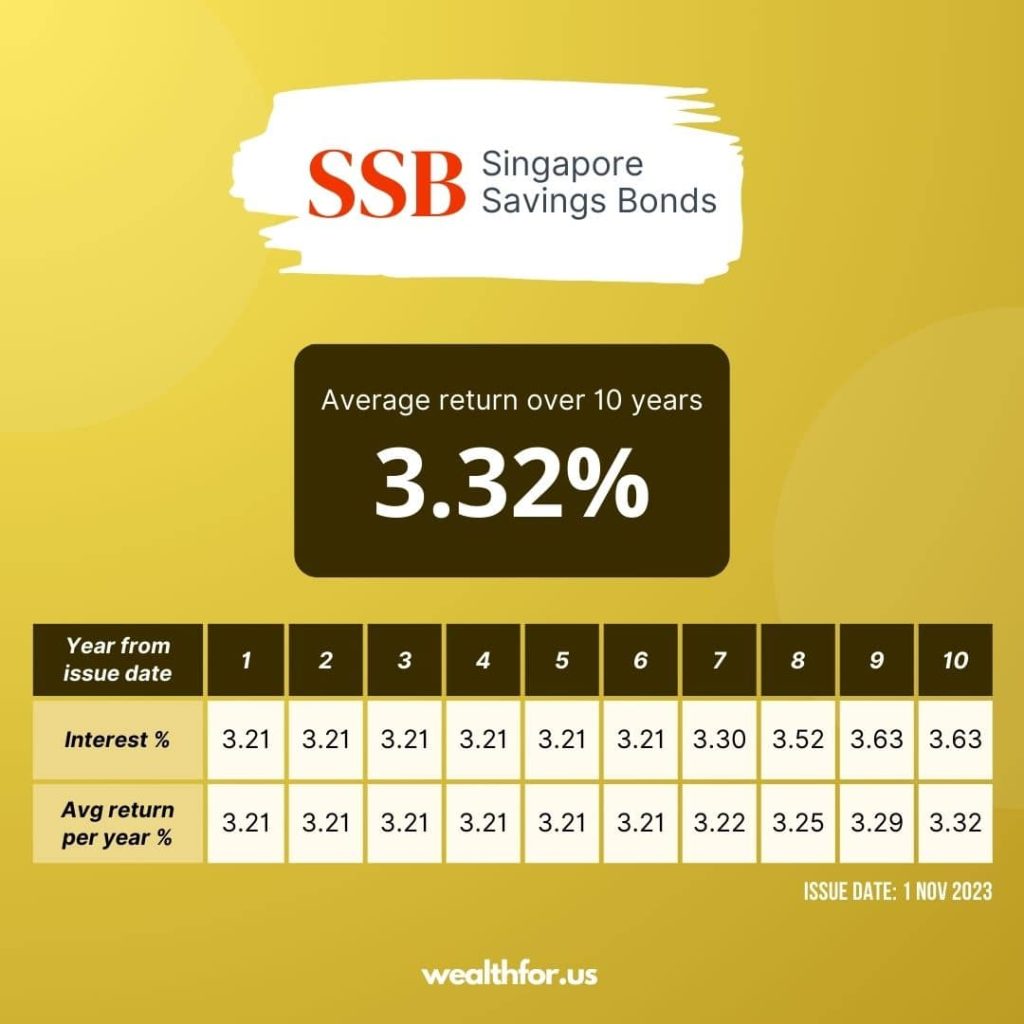

MAS has released the latest offering for Singapore Savings Bond SSB Nov 2023 (SBNOV23 GX23110V): 10-year average return of 3.32% and first-year return of 3.21%. These rates are a significant step up from the previous offering of ‘only’ 3.16% for the 10-year average rate. With the interest rates comfortably above 3%, is this the time to consider SSB again for our income portfolio?

Key Takeaways

- This SSB Nov 2023 has one of the highest rates in recent times. The 10-year average is 3.32%, and the first-year rate is 3.21%. We think this is quite an attractive offering for income-seeking investors.

- The market projects the interest rates to have already peaked and may start reversing down toward the latter half of next year. This month could be our chance to lock in the higher rates for the next ten years.

- For existing SSB holders, you may also recycle your older SSBs if they yield much lower than this month’s rates. The amount offered for this month is higher at $1 billion, so hopefully, this can lower the chance of oversubscription.

SSB Nov 2023 Details

In our opinion, this month’s offering is quite attractive! With the 10-year average rates at 3.32% and the first-year rate at 3.21%, this SSB Nov 2023 offering is among the highest in recent times. We have seen the trend of rising interest rates in the past few months, and it is no surprise that this month’s offering offers such a high interest.

For income-seeking investors, you may consider this month’s SSB to lock in the higher interest rates for the next ten years. The application timeline is as follows:

If you want to apply for this upcoming SSB, please do so before 26 Oct 2023. You may use any local bank’s online banking platform to submit your application. You may follow our step-by-step guide on how to buy SSB.

Is SSB Offering Competitive?

This offering is quite competitive because the rates are among the highest in recent years. Let’s look at the data to confirm this assessment.

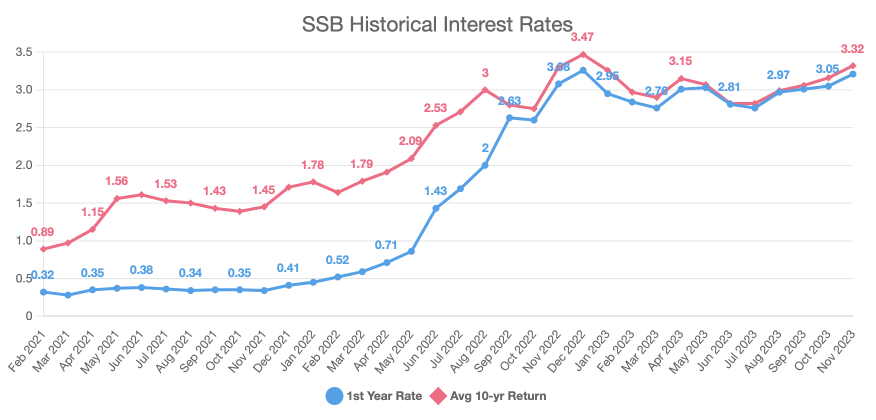

Where Do the Current Rates Stand Historically?

We have compiled historical SSB interest rates and summarized them in this graph below:

The chart shows that this SSB Nov 2023 offers one of the highest rates for both the 10-year average and the first-year rates. The current rates are much higher than the rates offered two years ago. Based on the recent historical data, we can safely conclude that this month’s rates are competitive.

What About Future Rates?

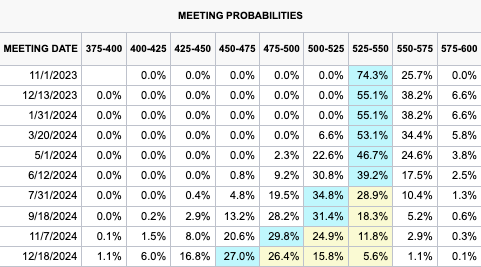

But what about if the interest rates continue to climb further? Even if we are already at a relatively high level, it doesn’t mean the interest rates won’t keep going up, right? Yes, possibly, but nobody knows with certainty, not even the Fed. Alternatively, we can look at what the market expects for future interest rate movements to get a general idea of which way rates are headed:

The market expects the interest rate to have peaked before starting to reverse toward the latter half of next year. The good news is that the 2024 end-of-year rate is still projected to hover around 50-75bps lower than the current level. It’s a bit lower, but not too significant.

The Fed also projects just one more additional rate hike before reversing towards the latter half of next year. The Fed is also expecting the rates to stay elevated for longer.

The market and the Fed agree that interest rates are nearing the end of their current upward trend and will likely begin to reverse sometime next year.

What do you think? Do you agree with the market and the Fed? If yes, maybe this is an excellent time to start locking in the higher rates for the next ten years and enjoy the ‘almost’ risk-free investment with a decent return. Even if the rates continue to climb, you can always recycle your SSBs to new ones.

Who Is SSB Suitable For?

SSB is a Singapore government bond guaranteed by the credit of the Singapore government. The Singapore government holds the highest credit ratings in the world; therefore, this investment is considered one of the lowest-risk investments in the market. With such a low-risk profile, SSB suits investors who seek capital preservation while still earning regular payouts.

SSB also allows investors to withdraw at any month without penalty. You even earn the accrued interest for the month. This additional liquidity benefit may suit investors who plan to use SSB to park their short-term cash.

Recycling Older SSBs

If you already have existing SSBs but with lower rates, this SSB Nov 2023 offering may be a chance for you to recycle those older SSBs. The amount offered is $1 billion, up from $800 million last month. Hopefully, with the higher offering amount, there is less chance we will get an oversubscription this month.

That said, there is a good chance more investors will be attracted to this month’s offering due to the higher rates. You can keep this in mind when you want to recycle your older SSBs to ensure that you take into account the possible allocation ceiling.

What Would We Do?

Taking Advantage of Yield Curve Inversion

If you have been following us, you should know that our current yield curve is inverted, meaning the shorter-term rates are higher than the longer-term ones. For example, the latest 6-month T-bill, considered short-term rates, yielded 4.07%, while this SSB offering only offers 3.32% for the average 10-year rate.

We want to take advantage of this inverted yield curve by investing our short-term cash into short-term investments with a similar risk profile to SSB. We use T-bill and high-yield savings accounts for our short-term needs.

Locking In Higher Rates

However, with the interest rates likely to start reversing next year, we would also like to lock in the higher rates for the next ten years. As such, we will recycle some of our older SSBs into this month’s offering to lock in the higher rates. By mixing the short and long-term rates, we can benefit from the higher short-term rates while still locking the long-term rates today while they are still relatively high.

Follow us to stay updated with the latest insights:

The latest SSB yields 10-yr avg of 3.32%. Wow!

The first year rate is 3.21%.

The amount offered is higher at $1 billion. This can be your opportunity for recycling older SSBs (if you have any).

If you are interested, do apply before 26 Oct 2023. pic.twitter.com/6fLscTnhyW

— wealthfor.us (@wealthfor_us) October 2, 2023