Keppel REIT has released its Q3 2023 business update, and let’s see how they performed this last quarter. Keppel REIT is an office-focused REIT with exposure to Singapore, Australia, South Korea, and Japan. Let’s dive into Keppel REIT Q3 2023 results.

Financial Highlights

In the following table, we compare the financial performance between the first nine months of this year to the same period of last year.

| 9M 2023 | 9M 2022 | Change | |

|---|---|---|---|

| Property Income | $172.6m | $164.4m | +5.0% |

| Borrowing Costs | ($48.8m) | ($40.5m) | 20.3% |

| Distributable Income from Operations | $148.6m | $165.4m | (10.1%) |

Property income for 9M 2023 increased by 5% compared to the 9m 2022 period. The increase is attributed to the higher rental income and increased portfolio occupancy from its Japan portfolio, KR Ginza II, which climbed to 74.5% (up from 36.3% in Q2 2023).

The higher income is offset by the higher borrowing cost, which climbed 20.3% to $48.8m. As a result, the distributable income from operations declined by 10.1% to $148.6m.

The overall financial result is within our expectations, where the borrowing cost is expected to grow significantly due to the higher interest rate environment. There is only a minimal amount of debt left due for refinancing in 2023, so the impact for the rest of this year should be limited. However, for 2024 and 2025, an additional 22% and 21% worth of debt must be refinanced. Should the high-interest rate environment persist for the next two years, Keppel REIT’s bottom line will have an additional impact as the borrowing costs grow.

Debt Profile

We recently paid more attention to REIT’s debt profile because of the pro-longed higher interest rate environment, which may cause refinancing large amounts of debt to be costly. We favor REITs with more prudent capital management to ensure they can weather this restrictive economic condition. Here is the summary of Keppel REIT’s Q3 2023 debt profile:

| Q3 2023 | Q2 2023 | Change | |

|---|---|---|---|

| Aggregate Leverage | 39.5% | 39.2% | +0.3% |

| Adjusted ICR | 2.9x | 3.0x | -0.1x |

| All-in Interest Rate | 2.85% p.a. | 2.84% p.a. | +0.01% |

| Weighted Average Term to Maturity | 2.7 years | 2.9 years | -0.2 years |

| Borrowings on Fixed Rates | 76% | 76% | N/A |

Generally, we can see that Keppel REIT’s debt profile has weakened slightly this quarter. The aggregate leverage ratio increased by 0.3% to 39.5%. This is still much lower than the regulatory limit of 50%. The adjusted ICR also declined slightly from 3.0x to 2.9x this quarter.

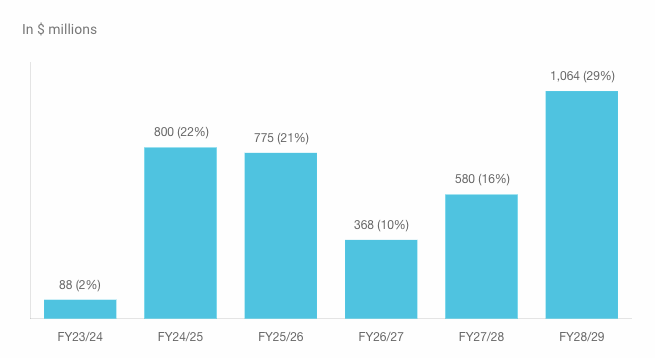

Debt Maturity Profile

The good news is that only a minimal amount of debt is due for the remainder of this year. However, for FY2024 and FY2025, there are 22% and 21% worth of debt to refinance. Although we believe we are reaching the tail end of this rate hike cycle, there is still a good chance that interest rates may stay elevated next year. Should this higher interest rate environment persist, Keppel REIT’s borrowing cost will continue to climb in the next two years due to this incoming refinancing needs and may impact future DPUs.

Regardless, we think Keppel REIT’s debt profile is still considered healthy and should be able to weather the pro-longed higher interest rate environment.

Portfolio Occupancy

Here is the summary of the key metrics:

| Q3 2023 | Q2 2023 | |

|---|---|---|

| Portfolio Occupancy | 95.9% | 94.9% |

| WALE | 5.6 years | 5.7 years |

The portfolio occupancy climbed this quarter to 95.9%, while the WALE declined slightly to 5.6 years. The higher occupancy is good news because this indicates the fundamental of the REIT is still strong. We also saw that Japan’s portfolio (KR Ginza II) started contributing more to the rental income this quarter as the occupancy climbed from 36.3% to 74.5%.

Singapore occupancy stayed resilient last quarter and climbed higher to 95.3%. The not-so-good news is that its Australia portfolio occupancy rate continued to underperform, only at around the 75-85% range. We believe the occupancy rate may improve when Australia’s prime office and commercial real estate market recovers.

Lease Expiry Distribution

The lease expiry distribution is well-staggered, with 13.3% due in 2024 and 14.9% in 2025.

Remarks

Keppel REIT Q3 2023 results showed a slight deterioration in its debt profile, which was still within expectations. With the interest rates at a decade high, it is no surprise that the borrowing costs shoot up significantly, thus impacting the distributable income.

However, with the underlying portfolio occupancy at a healthy level, the aggregate leverage ratio, and the adjusted ICR being far from the regulatory limit, we believe Keppel REIT should be well-equipped to weather any prolonged restrictive environment.

Keppel REIT also has a low Price-to-Book (P/B) ratio of only 0.59 and a dividend yield of 6.9%, which may be an appealing entry point for some investors willing to take on the risks associated with this REIT.

If you want more information about Keppel REIT, please visit our Keppel REIT analysis page and our Keppel REIT dividend page.

For analysis on other REITs, you may check out our Singapore REITs’ data page.

Related pages: