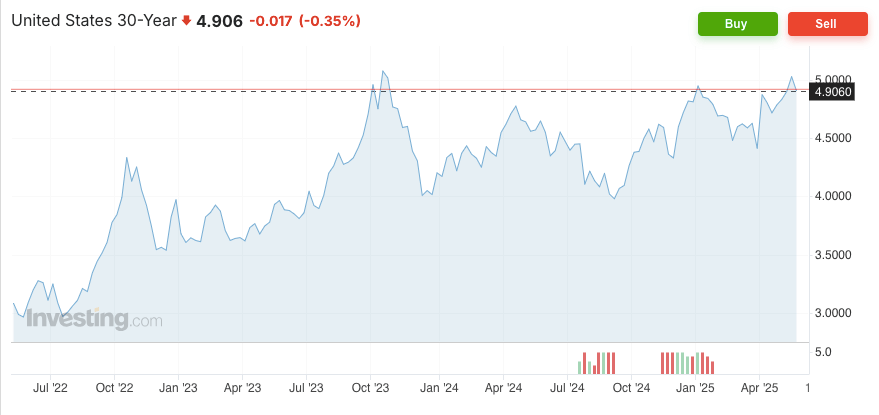

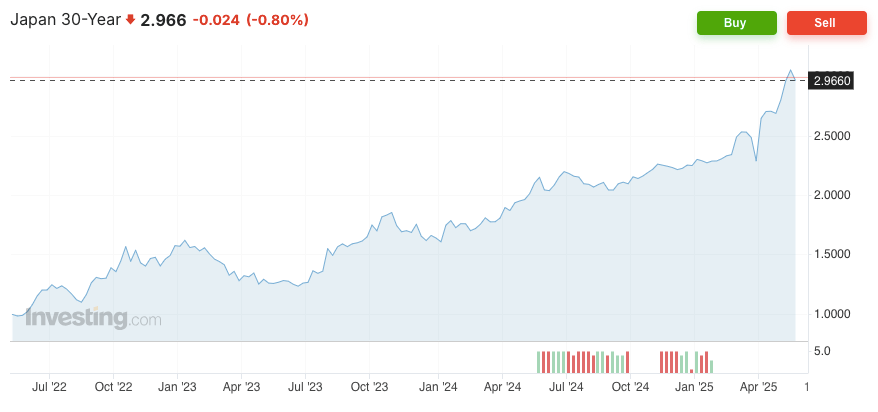

The global bond market has shifted, with yields rising across many developed nations. The US 30-year bond yield is approaching 5%, with the upward trend persisting. We can see a similar trend for Europe and Japan. What’s happening?

What Happened?

With inflation going down and fewer uncertainties about the US tariff policy, the expectation of further inflation should gradually diminish. Yet, the bond market keeps rising, with the US 30-year yield breaking 5% recently.

US Treasury Auction Performed Badly

The simplest explanation for why bond yields go up is that there is less demand for bonds. With lower demand, the yield needs to increase so that more investors are interested in the bond. For example, if a 4.5% yield is not attractive enough, a 5% yield may become attractive enough for some investors.

We recently saw tepid demand for the US Treasury 20-year bond, which breached the 5% yield mark. Granted, a 20-year bond is not the most popular, but the slow demand still shows the overall trend.

The free market is ultimately a function of supply and demand. Higher demand means higher price and lower yield, while lower demand means lower price and higher yield.

US Debt Soaring and Trump’s ‘Big Beautiful’ Bill

US government debt has reached a very high level and will become unsustainable unless the government changes its revenue generation or spending habits. Most investors should already be aware of this situation.

The US national debt currently stands at around $36.2 trillion, representing ~120% of the US GDP. The bad news is that at the beginning of 2024, the debt was only $34 trillion, which means the debt is increasing by trillions within a few months. This rate of increase is unsustainable.

Moody’s recently downgraded the US government, stripping it of its Aaa rating, although it remains an investment grade.

Additionally, Trump recently introduced a ‘big beautiful’ bill with tax cuts that can add another $3.8 trillion to the national debt.

Japan Bond Yield Rising Fast

Not only the US, but also the Japanese bond yield has been rising recently.

Japan has been in a deflationary economy for decades, but this may end soon as inflation picks up.

The increase in yield partly reflects expectations of higher future inflation and the burden of the Japanese government’s substantial national debt.

The potential unwinding of the Yen carry trade is a key concern arising from increasing Japanese bond yields. For years, investors have profited by borrowing at near-zero interest rates in Yen and investing in higher-yield assets abroad, notably in the US.

However, as Japan’s decades-long low-interest rate environment concludes, this arbitrage becomes less appealing. A continued rise in Japanese interest rates would heighten the risks of this Yen carry trade being unwound.

REITs Correcting

REITs are highly leveraged, and increasing interest rates result in higher borrowing costs for refinancing their debt. Recently, we have observed a slight correction in Singapore REITs as a market response to the uncertainties surrounding the increase in global bond yields. Singapore REITs with exposure to international markets may face additional uncertainties.

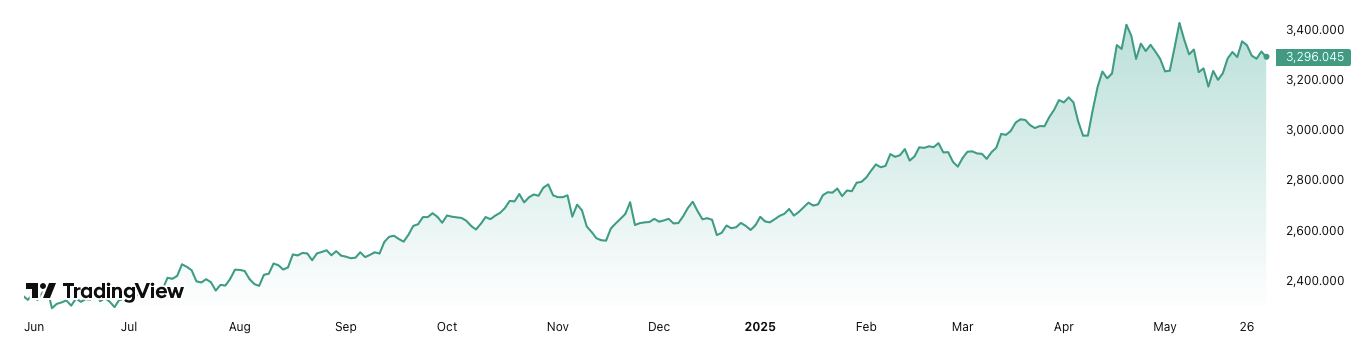

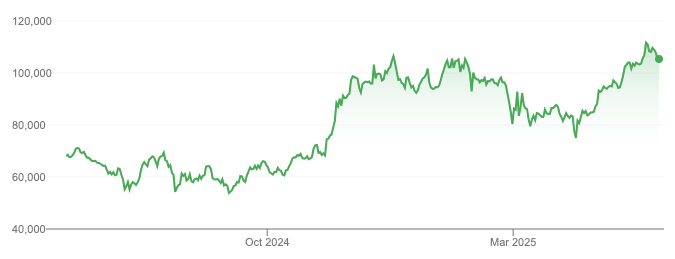

Gold and Bitcoin Rising

With the US national debt on an unsustainable path, investors are asking how exactly the US government will be able to pay down its debt. What if the US government tried to pay off its debt by inflating it away, printing its currency, and inducing inflation that would reduce the debt? The yield on US bonds may not be sufficient to compensate for the risks of default or inflation.

One way to mitigate risks is to avoid fiat-based instruments and invest in hard assets such as gold. Gold has been rising recently, breaking through its all-time high level.

Bitcoin, which is dubbed the digital gold, has also been performing very well, breaking all-time highs. It is another instrument with a fixed amount that cannot be printed out of thin air.

What Would We Do?

Generally, we do not prefer investing in long-term government bonds as their yield may not compensate for the risk of inflationary pressure of the fiat system. Short-term government bonds up to a few years may still be a decent choice for investors looking for regular income.

We do not think the US government will default on its debt anytime soon, but we are also not too confident that it will not inflate its fiat currency to lower its debt burden. As such, our preference stays the same, for long-term investment, we prefer to invest in hard assets (such as gold, bitcoin, real estate) or productive assets (such as stocks).