Hong Kong and Chinese stock markets soared recently after the Chinese government released an ‘aggressive’ stimulus plan that excited investors. After years of underperformance, the Chinese market finally showed a sign of a rebound. Should we look into the Chinese stock market now to ride the momentum?

New China Stimulus Measures

Chinese policymakers have finally introduced a series of bold stimulus measures to reignite the economy. These include cutting interest rates, the banks’ reserve requirement, the 7-day repo rate, the costs of existing mortgages, and the downpayment for a second home, as well as other fiscal stimuli to inject more liquidity into the economy.

Many analysts believe this measure has a different tone than the earlier measures, which tend to be underwhelming.

The million-dollar question is whether the Chinese government’s implementation and follow-up on this stimulus plan will sufficiently boost the economy.

A New Bull Market?

The government crackdown and the policy changes in the real estate sector introduced the multi-year bear market in the Chinese stock market in the past few years. This bear market taught investors one crucial lesson: the Chinese policymakers have a strong influence on the stock market. This is the risk that investors need to be comfortable with when investing in the HK/China market.

Conversely, policymakers can also have an outsized influence if they want to support their economy. Investors are watching policymakers’ moves to see if they are now ‘serious’ about stimulating the economy with their monetary policy and fiscal stimulus.

We think the market’s direction may depend on whether or not the government implements its stimulus measures as strongly as the market expected. We do not think monetary policy alone is sufficient to stimulate the structural decline in the Chinese economy, and a form of sustained ‘big bang’ fiscal stimulus is likely needed to ignite the economy’s growth again.

So far, we know that cutting banks’ reserves requirement will inject up to 1 trillion yuan in liquidity, but other fiscal numbers have yet to be released, so let’s see how much fiscal injection we will see from the government this time.

That said, we have seen in the past that the details of the policies introduced by the policymakers have been underwhelming. Therefore, most past rallies have fizzled out as those measures were insufficient to lift the ailing economy.

Will this time be different? Given the broad measures the policymakers introduced in one go, there is a good possibility this could be ‘the one.’ The market seems to agree with this sentiment by rallying hard with the introduction of these new stimulus measures.

Market Valuation

The HK/Chinese stock market has been depressed recently, and its valuation was low. But after the recent rally, is market valuation still attractive?

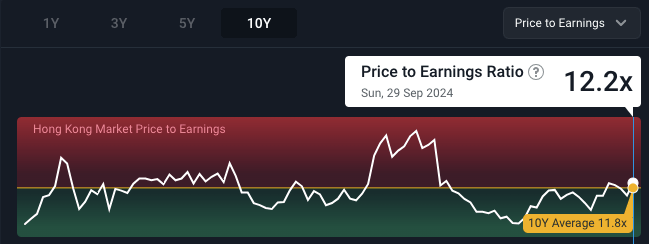

Let’s examine the Hang Seng Index, which comprises some of the largest companies on the Hong Kong Stock Exchange. As of this writing, the Hang Seng Index currently has a PE ratio of ~12.2x, slightly higher than its 10-year average of 11.8x. The index seems to have rallied enough to return to its average long-term valuation.

The chart shows that the index was below its long-term PE ratio average throughout 2022 and 2023 but has since reverted to its mean. From the PE ratio perspective, we can say that the market is not cheap but also not expensive at the current level.

However, please note that the PE ratio is a ratio of price divided by earnings, which means if earnings grow, the price will also increase even with the PE ratio staying the same. Because the company’s earnings have not been great recently due to the depressed economy, we can expect they will also start to grow as the economy recovers. So, even if the index is fairly valued in terms of the PE ratio, it doesn’t mean the index won’t rise as the economy and company earnings grow.

For perspective, the Hang Seng Index currently stands at a level we already saw in 2007. That’s more than 15 years of going nowhere. If the Chinese economy starts to recover well, the market may continue to rise in the years ahead.

What Do We Do?

We still believe that the Chinese economy will recover over the long term, regardless of whether or not this particular stimulus measure is ‘the one.’

Over the past few years, we have accumulated positions in the Hong Kong stock market, where many of the largest Chinese companies are listed. However, due to the policy risk associated with investing in China, we keep our Chinese positions smaller to manage our risk.

Given the recent strong rally, we are not rushing to add more positions to the HK/China market. However, we might consider adding more positions should there be a decent pullback. Remember, the stock market does not go up in a straight line; there are ups and downs. A pullback in a bull market can be an excellent opportunity to add to our positions.