The auction result for T-bill BS24113N concluded with a cut-off yield of 3.7%, a slight decline from the previous auction’s 3.74%. Did you manage to get your desired allocation?

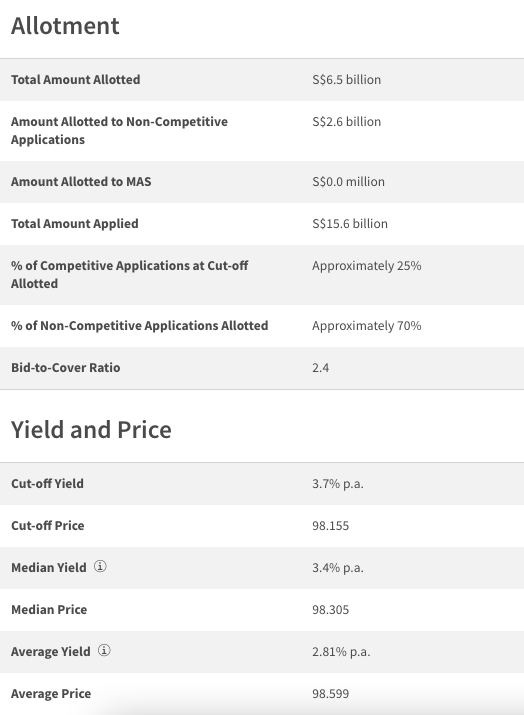

Auction Result

Please note that this T-bill BS24113N auction offered a slightly lower allotment of $6.5 billion, down from $6.6 billion in the previous auction.

Here is the result summary:

Yield Fell Slightly

The yield on this T-bill BS24113N declined slightly but stayed relatively steady at 3.70%. The previous auction saw the yield at 3.74%. Despite the decline, the current T-bill yield remains among the highest in recent years.

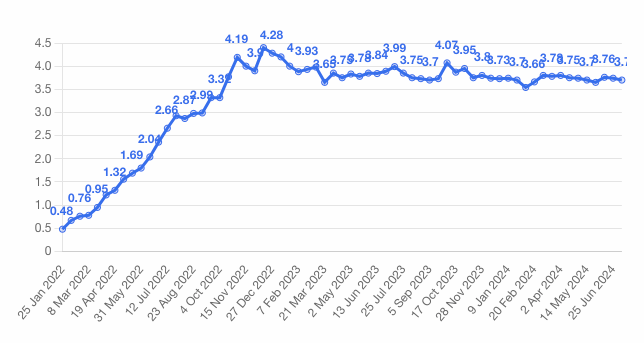

The above chart shows the historical T-bill yield chart back to early 2022. The yield was still below 1% then! The current yield of 3.70% has been in the range we have been in since early 2023. The question is, how much longer will we see this higher yield?

While there is no way to predict with certainty, we can see where the Fed and the market expect interest rates to go.

The chart above shows where the market expects interest rates to be for the next several months. The market expects interest rates to reverse toward the end of this year and even further rate cuts in 2025. The Fed has also hinted at possible rate cuts toward the end of this year.

Do you agree with this expectation? If so, now can be your opportunity to lock in the higher rates while they last.

Demand Climbed Further

We saw yet another high-demand auction, this time for T-bill BS24113N, at $15.6 billion. This is even higher than the previous auction’s $15.5 billion, which recorded a jump of $1.3 billion! This higher demand can be attributed to the relatively higher yield from T-bills and the lack of alternatives for short-term ‘almost’ risk-free investment.

We also witnessed another elevated demand from non-competitive bidders as the cap was hit again. Non-competitive bidders only got ~70% of their allocation. This trend of higher non-competitive bids has been occurring for quite a while, so if you want to ensure that you can secure your full desired allocation, competitive bids may be the option that you should consider.

Alternatives

As mentioned, T-bills have had little competition recently, as alternatives with similar risk profiles offer less competitive rates. Let’s look into some of them.

Fixed Deposits

Fixed deposits have been one of the more prevalent alternatives to T-bills due to their short-term nature and guaranteed rates. Unfortunately, fixed deposit rates in Singapore have not been too competitive recently. As of this writing, the best 6-month fixed deposit rate is 3.35%, offered by CIMB Bank. The best 3-month fixed deposit rate is 3.5%, provided by the Bank of China. Yeah, they could be more competitive.

Cash Management Accounts

Although their risk profiles differ, we also like to look into cash management accounts with guaranteed payouts, such as Syfe Cash+ Guaranteed or StashAway Simple Guaranteed. Both offer 3.6% for the 6-month lock-in period. Now we are talking! They are pretty competitive compared to T-bills.

There is also a new contender in this space: Chocolate Finance, which runs a promotion offering a fixed return of 4.2% for the first $20,000 deposit and a $3.5 % target rate after that. There is no lock-in period.

If you are interested in cash management accounts, please remember that they are considered investments and not insured by the SDIC.

Singapore Savings Bonds (SSB)

SSB has seen quite attractive rates recently. This month’s SSB offers 3.22% for its 10-year average and 3.19% for the first-year rate. These rates are competitive, considering SSB locks in the rates for ten years. If you think interest rates may start to reverse soon, it may be worth considering locking in these higher rates for longer by getting into longer-duration investments such as SSB.

What Would We Do?

We have been parking our short-term cash allocation into T-bills and will likely continue to do so while these higher rates last. However, as we believe the current interest rates may have peaked and may start to reverse soon, we have migrated some of our short-term cash allocations from T-bills to SSBs to lock in the higher rates for much longer.

If you are interested in applying for the next T-bill auction, you may follow our guide on how to buy T-bills.

If you plan to apply with CPF, you can estimate the additional interest you may earn using our CPF T-bill calculator.