Asset is something we own, and liability is something we owe. That is what the dictionary says. But what does it mean in the context of wealth building?

Robert Kiyosaki, the best-selling author of ‘Rich Dad Poor Dad’ once said: “The rich buy assets. The poor only have expenses. The middle class buys liabilities they think are assets.”

Yes, unfortunately, Robert Kiyosaki is correct. Many people still confuse liabilities with assets. Are you one of them?

In this article, we would like to present an alternative definition for assets vs. liabilities that is more suitable for wealth building. And no, it is not the same as how Robert Kiyosaki defines them.

What are assets and liabilities?

- Asset is something (that you own) that increases your wealth over time.

- Liability is something (that you own) that decreases your wealth over time.

That is it, a very simple definition.

Let us take a look at some common examples:

Car

To determine whether a car should be considered an asset or liability, we can ask a simple question: By buying a car, will your net worth increase over time?

Owning a car also means paying regular maintenance costs such as insurance, gas, etc. Car will also depreciate over time. By buying a car, your net worth will likely decline year over year. By our definition, car is a liability.

However, if your car is being rented and earning more than the monthly cost and the depreciation, you may consider your car as an asset.

Real-estate property

Property usually appreciates over time (thanks to inflation!). However, owning a property also means paying monthly costs, such as taxes, maintenance fees, water & electricity bills, etc. If the price appreciation is faster than the monthly costs, you can consider your property an asset. You may also offset those monthly costs by renting your property.

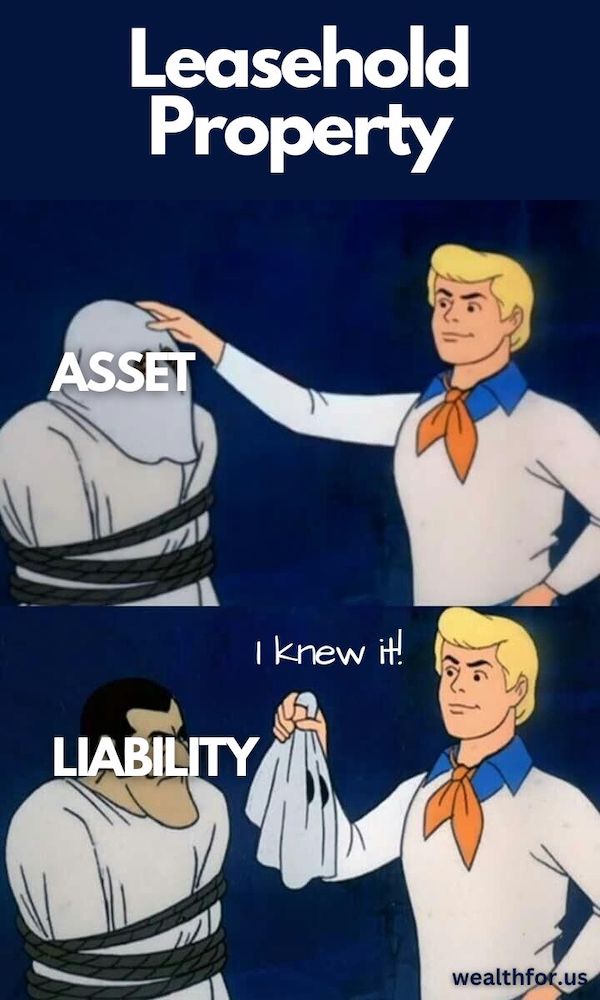

Now, let’s get into a more controversial topic: How about leasehold property?

Leasehold property does not own the land it is built on. You are just renting the land. Once the lease expires, you can no longer stay there. Leasehold is the common property type in some countries such as Singapore, China, etc.

Is leasehold property an asset? Let us ask the same question: Will buying leasehold property increase your wealth over time? Since the price of the leasehold property depreciates as the lease gets closer to expiry, the property price appreciation may not be enough to offset the depreciation as it nears expiry. Thus, we can consider leasehold property as a liability.

If you have rental income from the property, and the rental is enough to cover the depreciation of the property value, then you can consider it as an asset. Please note that this may be hard to achieve as the lease gets closer to expiry. The decline in value usually accelerates closer to the lease expiry.

Precious metals

Although precious metals (such as gold and silver) do not generate additional income for you, they usually appreciate over time (again, thanks to inflation!). Thus, we can consider precious metals as assets.

Stocks

Stocks expected to appreciate can be considered assets. However, not all of them are the same. If you buy speculative stocks that are likely to shrink in value (or even go to bankruptcy), they can be considered liabilities.

Digging deeper into assets and liabilities

As you can observe from the examples above, not all assets and liabilities are created equal. We can further break them down as follows:

Productive assets

Income-producing assets that bring more money into your pocket (ex: cash, rental income, dividends). Examples: rental properties, stocks, businesses, etc. Acquiring these assets may accelerate your wealth accumulation due to the effect of compound interest.

Non-productive assets

Assets that do not produce anything but are expected to appreciate over time. Note that this is only an expectation because we cannot guarantee how an asset will perform in the future. Examples of non-productive assets are gold, silver, arts, antiques, etc.

Liabilities

Some liabilities regularly take cash out of your pocket, such as car, iPhone, etc. Some do not have regular costs but are still expected to lose value over time. Examples of liabilities are furniture, TV, computer, etc.

Wait… Objection!

“But we are in the 21st century, I need my smartphone, laptop, TV, and these are all liabilities, so how?” 🙁

Chill chill… If you cannot live without them, then get them. We are not saying you cannot have them, but we recommend you keep your liabilities to a minimum. The more income you can allocate to acquiring assets, the faster you can build your wealth.

What should I do?

The goal is always to grow your wealth, so with that in mind:

- Always try to increase your assets while reducing your liabilities

- When you receive your paycheck, you want to spend most of it on acquiring assets (and not liabilities).

- Rinse and repeat! Accumulate enough assets such that the value generated by your assets (rental income, stock dividends, interest) exceeds your cost of living. Once you achieve this, you are financially independent.

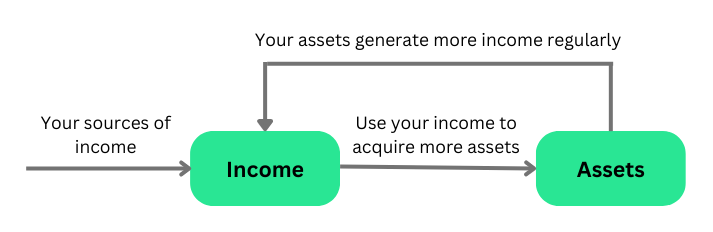

The diagram above illustrates how having assets can help increase your income. As you acquire more assets, you will earn more income from your assets, which you can use to acquire even more assets.

Surround yourself with assets, not liabilities

Understanding the difference between assets vs liabilities is the secret to building wealth. We also hope that you have enough understanding of how assets can help you accelerate your wealth building.

To conclude this article, we would like to invite you to answer these self-evaluation questions:

- What was your last major purchase? Was it an asset or a liability?

- How much of your income do you use to acquire assets vs liabilities?

If you find this article helpful, follow us and help us spread the knowledge by sharing this with your friends and family.